What if you found out that a single year of college could cost as much as a brand new car?

A year at a US university costs around $25,000 on average, which means a four year degree could cost $100,000. While that number looks huge, families use tools like compound interest and special savings accounts to make it manageable by starting early.

A year at a US university costs around $25,000 on average. That means four years of studying could cost $100,000. If you live in the UK, the cost for tuition alone is usually around £9,250 per year, but when you add in rent and food, the total price tag is much higher.

In the United States, the 'sticker price' of college often includes more than just classes. It covers your room (where you sleep), your board (what you eat), and even your books and lab fees. That is why the total can be so high!

These numbers sound impossible to save all at once. However, the secret is that most families do not save the whole amount in a single year. Instead, they use the power of time to build a college fund slowly, often starting from the day a child is born.

Why Starting Early is a Superpower

When your family saves for college, they are usually doing more than just putting cash in a box. They are putting money into accounts that earn interest, which is extra money the bank or an investment fund pays you for keeping your money there.

An investment in knowledge pays the best interest.

This leads to compound interest, which is when you earn interest on your original money, and then you earn interest on that interest. Over 18 years, compound interest can do about half the work for you. If a family saves a little bit every month for a long time, the total amount grows much faster than if they tried to save a lot of money right before college starts.

Finn says:

"Wait, if the bank is paying me interest, does that mean I get free money just for leaving my college fund alone?"

How Families Actually Save

Most families use special accounts designed just for education. In the United States, the most common tool is a 529 plan. This is a special type of account where the money can grow without being taxed, as long as the money is used for school expenses like tuition or books.

In the United Kingdom, many parents use a Junior ISA. This is a long-term savings account where the money belongs to the child, but they cannot touch it until they turn 18. Because the money is locked away for so long, it has plenty of time to grow through the stock market or high interest rates.

In a 529 or Junior ISA, your money is often invested in the stock market. This means it can grow much faster over 18 years, but it can also go down in value sometimes.

In a regular savings account, your money is very safe and will never go down, but it grows much slower because interest rates are usually lower.

Some families also use regular savings accounts or investment accounts. While these do not always have the same tax benefits, they are flexible. No matter which account a family chooses, the goal is the same: to have a dedicated place where the principal, or the original money put in, can stay safe and grow.

The best way to save for college is to start when your children are young. If you haven't started yet, start today.

The Monthly Math of Saving

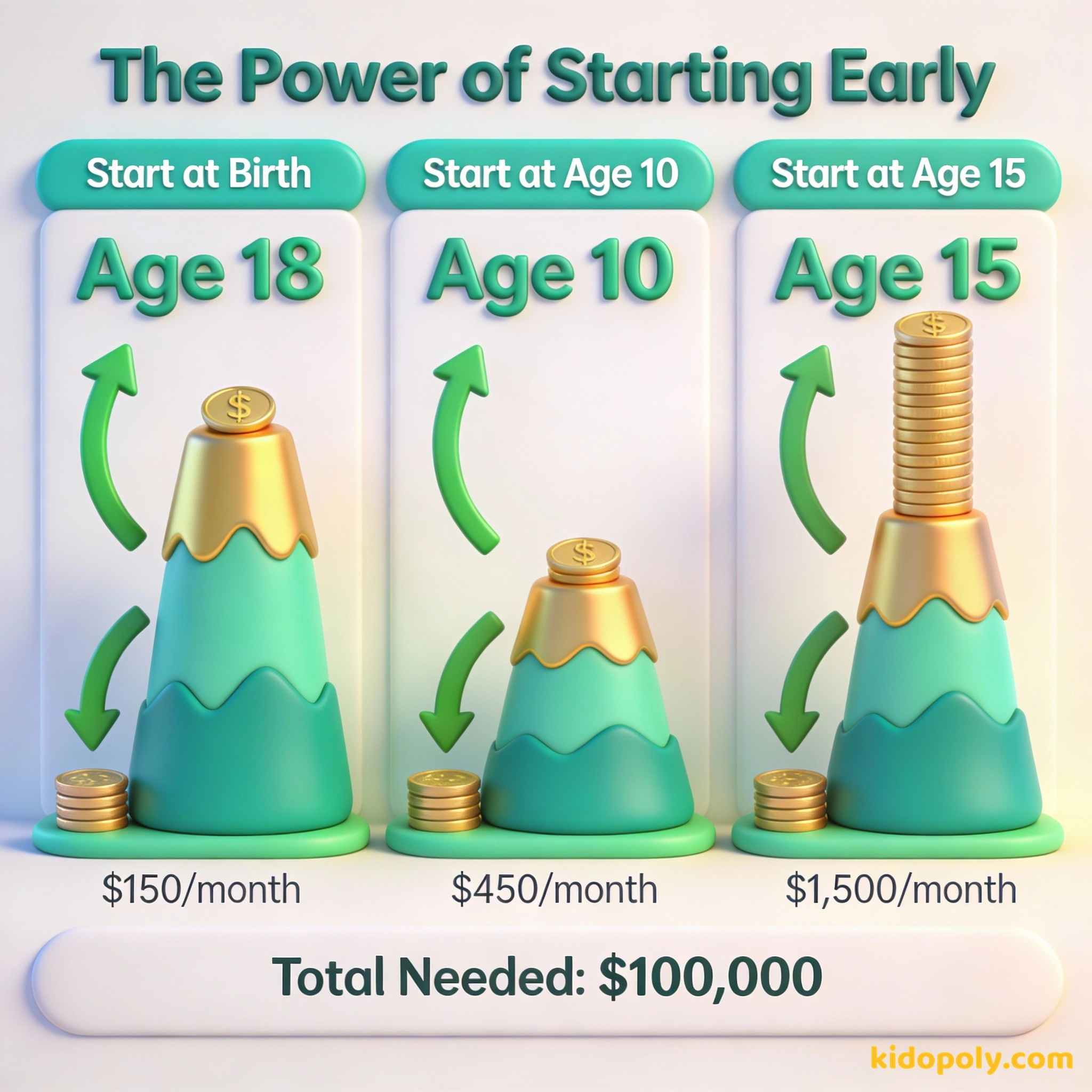

How much does a family actually need to put away? The answer depends entirely on when they start. If a family starts the day you are born, they have 216 months to save before you finish a four-year degree. If they wait until you are 10, they only have 96 months.

To save $100,000 for college by age 18 (assuming 6% growth): - Start at Birth: $235 per month - Start at Age 6: $410 per month - Start at Age 12: $950 per month - Start at Age 16: $3,800 per month Starting early makes the monthly cost over 16 times cheaper than starting late!

As you can see, waiting even five years can double the amount of money a family needs to find in their budget every month. This is why financial educators always say the best time to start was yesterday, and the second best time is today.

Mira says:

"My parents told me that saving for my university is like planting a tree. We had to plant it years ago so it would be tall enough to climb by the time I am ready!"

How Kids Can Help

Saving for college is usually a team effort. While you probably cannot save $100,000 on your own by mowing lawns, you can play a big role in how the fund grows. Many kids decide to put a portion of their birthday money or holiday gifts into their college fund.

Imagine it is your 12th birthday. You receive $100 in cards from your relatives. If you spend it all on video games today, you have a new game. But if you put that $100 into a college fund that grows at 7%, it could be worth over $150 by the time you head to campus. You are literally paying your future self to go to school!

When you get a part-time job as a teenager, you might decide to save 20 percent of your earnings for school. Even if it is only $20 a week, that money has several years to earn interest before you need it. Plus, it helps you feel more connected to your future and the hard work your family is doing.

Price is what you pay. Value is what you get.

Other Ways to Pay

Saving is only one piece of the puzzle. Most students use a mix of four different things to pay for their education. Saving is the first, but the other three are also important to understand as you get older:

- Scholarships: Money given to you by a school or organization because of your grades, sports, or special talents.

- Financial Aid: Support from the government based on your family's income.

- Student Loans: Money you borrow from the government or a bank that you must pay back later with interest.

Mira says:

"It is cool to know that even my $10 from chores helps. It makes me feel like I am actually an owner of my own education."

Sit down with your parents and ask: 'Do we have a college savings plan?' You do not need to know the exact dollar amount, but understanding the strategy helps you plan your own future. You can even use an online 'College Savings Calculator' together to see how much your current savings might be worth when you turn 18.

By combining savings with these other options, the giant mountain of college costs becomes a series of smaller hills that are much easier to climb. The earlier you and your family start talking about it, the more prepared you will be when those graduation bells finally ring.

Something to Think About

If you could choose one thing to save for besides college, what would it be, and how does the scale of that goal compare to a university degree?

This is about your personal values and how you see the 'worth' of different big life goals. There is no right or wrong answer.

Questions About Saving

What happens to a 529 plan if I don't go to college?

Can I have my own savings account for college?

Is it ever too late to start saving?

Start Your Future Today

Saving for college is a long-distance race, not a sprint. Whether your family has been saving since you were a baby or you are just starting to talk about it today, every dollar counts. Now that you know how the math works, why not check out our guide on how savings-accounts-for-kids work to see where you can put your own contributions?