Financial Literacy Statistics 2026 - Key Facts and Trends

In a rapidly shifting economic landscape, understanding money is no longer just a 'nice-to-have' skill - it is a critical safety net for the next generation. While 88% of adults support requiring financial education in high schools, data from 2026 reveals that barely half of U.S. adults can answer basic questions about interest, inflation, and risk. For parents and educators, these numbers are a call to action: identifying the gaps today is the first step toward building a financially secure tomorrow for our children.

Key Takeaways

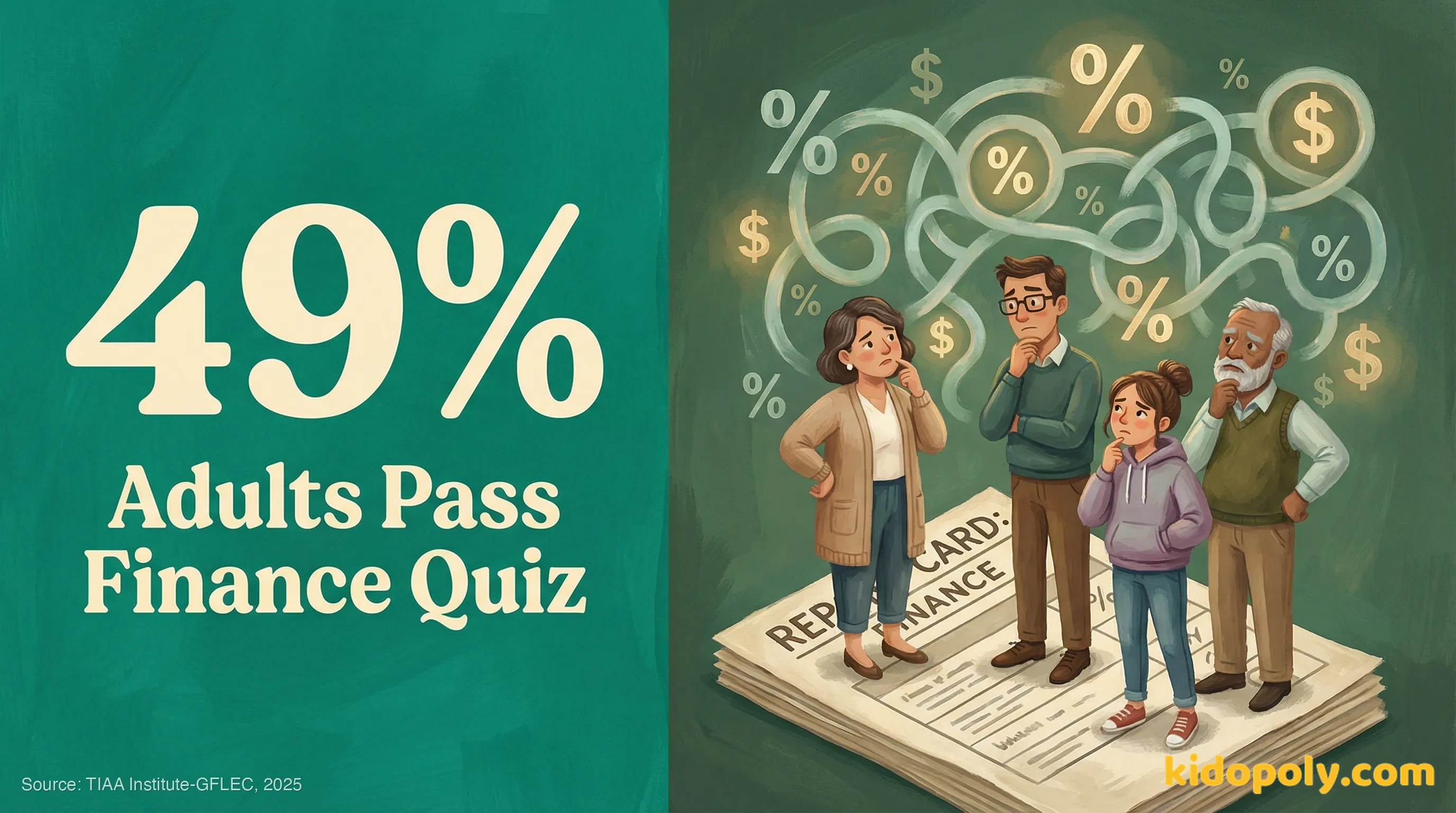

- Financial literacy has flatlined: Only 49% of U.S. adults correctly answered basic financial questions in 2025.

- Gen Z is struggling the most: Young adults (18-29) scored just 38% on financial literacy tests, the lowest of any generation.

- Education is expanding but unequal: 29 states now require financial education, but only 31% of teens report actually having access to a course at their school.

- The cost of ignorance is high: Lack of financial knowledge cost the average American an estimated $948 in 2025.

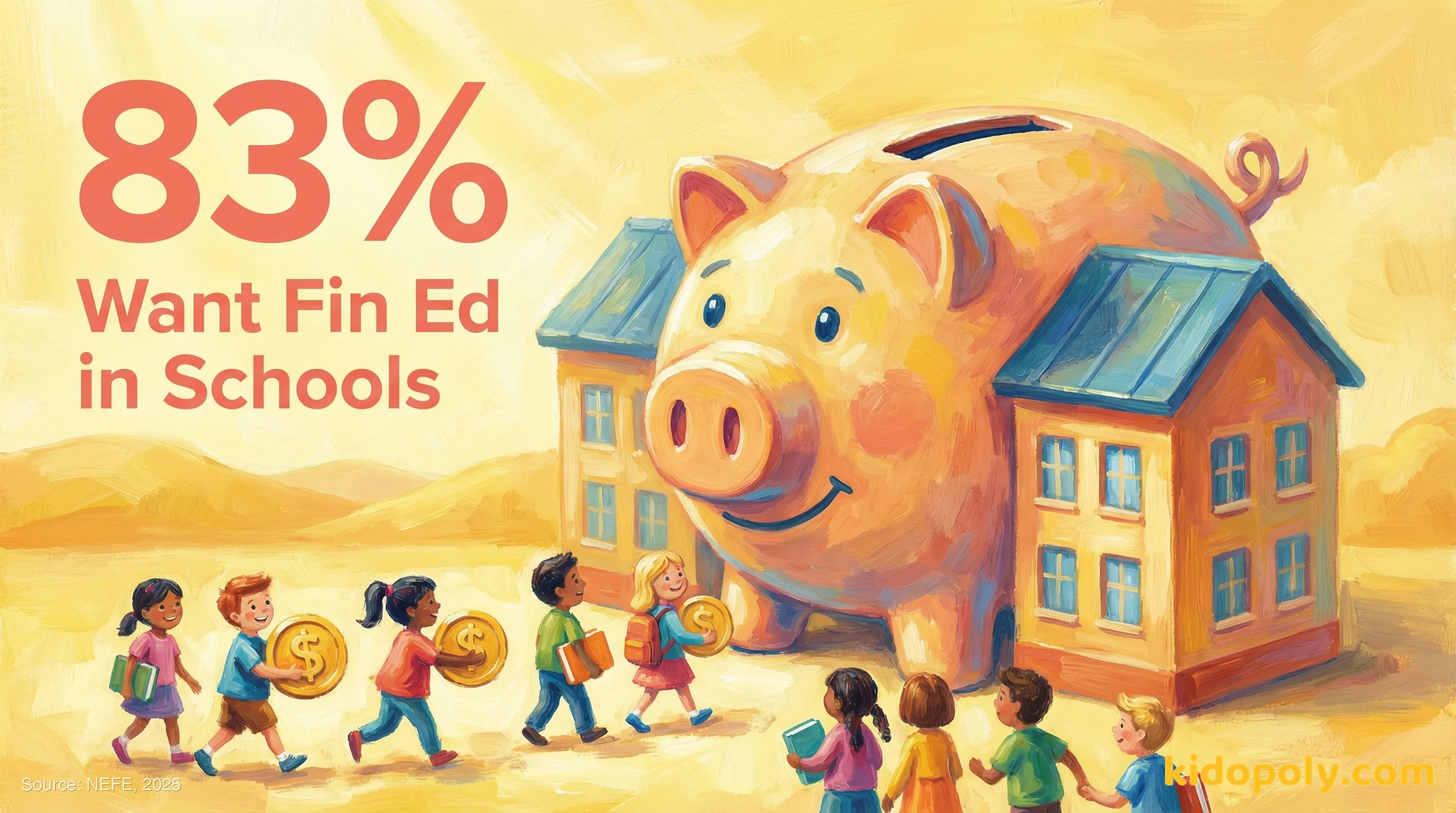

- Public support is overwhelming: 83% of adults believe their state should require a personal finance course for high school graduation.

The Big Picture: Financial Literacy in 2026

of U.S. adults correctly answered basic financial literacy questions

This figure has remained stagnant, hovering around the 50% mark for nine consecutive years.

Financial Literacy Scores by Generation (2025)

| Generation | Average Score (% Correct) |

|---|---|

| Gen Z (Ages 18-29) | 38% |

| Millennials (Ages 30-44) | 46% |

| Gen X (Ages 45-60) | 51% |

| Baby Boomers (Ages 61+) | 55% |

of Americans grade their own money skills as 'C' or lower

Low confidence often correlates with lower literacy scores.

Financial Education in Schools

guarantee a standalone personal finance course for high schoolers

As of August 2025, these states have passed legislation requiring a dedicated course for graduation.

Public Support for Financial Education (2025)

| Sentiment | Percentage |

|---|---|

| Believe state should require a course | 83% |

| Wish they had been required to take a course | 82% |

| Say their high school did NOT offer a course | 61% |

Source: National Endowment for Financial Education (NEFE) (2025)

Access to Guaranteed Financial Education by State Implementation (Top 5)

The Cost of Financial Illiteracy

Estimated average loss per person in 2025 due to lack of financial knowledge

Losses stem from high interest, fees, and fraud.

Financial Struggles by Literacy Level

| Financial Struggle | Likelihood for Low Literacy vs. High Literacy Adults |

|---|---|

| Constraint by Debt | 2x more likely |

| Financially Fragile (unable to find $2,000) | 3x more likely |

| Spend 20+ hours/week on money issues | 8x more likely |

Source: WealthWave: The Financial Literacy Emergency of 2026 (2025)

Does financial literacy actually reduce debt?

Demographic Gaps and Equity

Financial Literacy Scores by Demographic

Source: WealthWave: The Financial Literacy Emergency of 2026 (2025)

Women score below 25% on financial literacy tests

Compared to 1 in 7 men who score in this lowest quartile.

Why is there a gender gap in financial literacy?

Student Perspectives and Digital Trends

of teens would eagerly enroll in a financial literacy course

However, only 31% report having access to such a course at their school.

Source: Junior Achievement USA (2024)

Teen Financial Interests and Concerns

| Topic | Stat |

|---|---|

| Interested in Career/Entrepreneurship Courses | 60% |

| Likely to take course on Paying for College | 41% |

| Gen Z able to understand Cryptocurrency | 54% |

Source: Junior Achievement USA (2024)

Are kids learning about money from TikTok?

Common Questions from Families

When should I start teaching my child about money?

Does my state require financial education?

How do I know if my teenager is financially literate?

What Families and Educators Can Do

What Parents Can Do

- Start the conversation early. Don't wait for high school; research supports introducing concepts in elementary school to build a 'healthy money mindset' before bad habits form.

- Vet their digital diet. Since nearly 70% of Gen Z learns from social media, watch the videos they watch and discuss which advice is credible and which is risky 'finfluencer' hype.

- Advocate for your school. With 83% of adults supporting state requirements, use your voice at school board meetings to ask for standalone personal finance courses if your district doesn't offer them.

What Educators Can Do

- Integrate, don't just add on. Even if a standalone course isn't mandated, incorporate financial examples into math (interest rates) or social studies (economic history) lessons.

- Use free, high-quality resources. Organizations like the CFPB and Next Gen Personal Finance offer free curriculums and 'lesson playlists' that can be used in advisory periods or seminars.

- Focus on risk and safety. Data shows Gen Z scores lowest on 'comprehending risk.' Prioritize lessons on identifying scams, understanding high-interest debt, and digital security.

Sources (7)

- 1. TIAA Institute-GFLEC Personal Finance Index (2025) https://www.tiaa.org/public/about-tiaa/news-press/press-releases/2025/06-09

- 2. National Endowment for Financial Education (NEFE) (2025) https://www.nefe.org/news/2025/04/poll-majority-of-us-adults-want-financial-education-in-high-schools.aspx

- 3. Intuit Financial Literacy Ranking by State (2025) https://www.intuit.com/blog/global-stories/financial-literacy-ranking-by-state/

- 4. Junior Achievement USA (2024) https://jausa.ja.org/news/blog/teens-want-financial-literacy-education-but-many-schools-don-t-offer-it

- 5. Carry: How Financially Literate Is America (2025) https://carry.com/learn/how-financially-literate-is-america-key-stats

- 6. WealthWave: The Financial Literacy Emergency of 2026 (2025) https://wealthwave.com/allison/blog/the-financial-literacy-emergency-of-2026

- 7. WalletHub Financial Literacy Survey (2025) https://carry.com/learn/how-financially-literate-is-america-key-stats